Why We Use Credit Cards

to Travel as a Family

How we fund most of our family travel without spending more than we already do

How We Got Here

For years, we bought standalone travel insurance for every big-ticket trip — and those costs add up fast. At some point we found out about the Costco Citi Card, which came with travel insurance built in. When Costco later dropped that benefit, we went looking for a replacement and landed on the Chase Sapphire Preferred. At first the $95 annual fee felt weird — now it feels like one of the best $95 we spend all year.

Now most of our hotel stays and a good chunk of our flights are covered by points. We didn’t change how we spend — we just changed which card we put everyday spending on.

Where it clicked: Our first real test of this system was our Hawaii trip → That’s where we stopped “just using cards” and actually built a strategy around them. It’s still the trip that best shows what this can do for a family.

Why Do Credit Cards Make Family Travel Better?

The Part Nobody Talks About: Real Credit Card Insurance Wins

Everyone talks about points and sign-up bonuses. Almost nobody talks about the protections quietly built into cards you already carry — until something goes wrong. Here are three times those benefits put real money back in our pocket.

Aryan came down sick right before a getaway we’d booked — and the Airbnb was strictly non-refundable. We filed a trip cancellation claim through our Amex Platinum and got the full cost back, around $750. A trip we’d already written off as money lost, refunded.

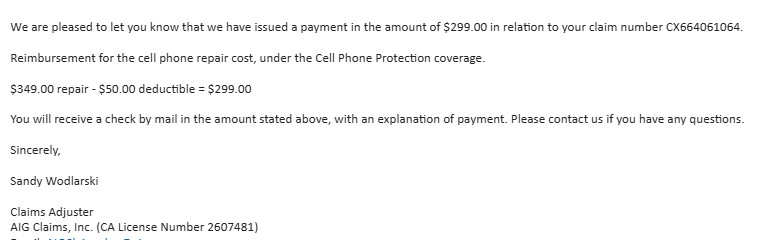

Pay your phone bill with the card and damage is covered — that’s the whole catch. We filed a repair claim and Amex reimbursed $299, for a benefit we never paid a cent extra for.

An appliance we’d bought on our Discover card failed after the manufacturer warranty ran out. It couldn’t be repaired, so Discover’s extended warranty benefit sent us a check for the full cost — $1,018 back, for a benefit we’d completely forgotten the card even had.

This Only Works If…

The Transfer Game

The basic move is cashing out points directly — simple and decent value. But the real leverage comes from transferring points to airline and hotel partners. That’s where a point can go from being worth 1 cent to 3–5 cents depending on the redemption.

It sounds complicated but you don’t need to master it overnight. Start with the Sapphire Preferred, learn the basics, and go from there. The resource that helped us most is Max Miles Points on YouTube — practical, up to date, and easy to follow.

And if you get stuck or just want a second opinion on a redemption, come say hi on our Facebook page — we’re always happy to help with points questions.

Example from our trips: Transferred 15K Amex points to Virgin Atlantic → booked round-trip Delta flights to Orlando for the whole family. Transferred 175K Hyatt points → 5 nights at the Hyatt Regency Maui with ocean view upgrade and club lounge access.

A Few Redemptions That Show the Magic

Numbers tell the story better than we can. Here are four redemptions where points turned a splurge into something we would never have booked in cash — the full play is in each trip guide.

Grand Hyatt Kauai

150K Hyatt points covered 6 nights at a resort that runs well over $500 a night in cash — with an ocean view upgrade and club lounge access on top.

✓ 6 nights on pointsKimpton Seafire Resort

One of the Caribbean’s most-wanted resorts. We went over spring break, when rooms were running about $3,000 a night — a cash total of $15,617. We booked it for 210K IHG points plus $340 in resort fees instead. Screenshots and the full breakdown are in the Cayman guide.

✓ $15,277 saved on one stay5 Nights in Banff & Kananaskis

Five Marriott Free Night Certs covered our peak-summer stays in Banff and Kananaskis — around $2,500 in cash rates we simply did not pay.

✓ ~$2,500 saved with certsNew Delhi → Chicago in Business Class

88K LifeMiles per person — a heavy points spend, but our first time flying business class. Lie-flat seats, multi-course meals, and pajamas the kids still talk about.

✓ Business class on pointsCredit Card Travel Rewards: Family FAQ

For us, yes — but only because all our accounts are set to auto-payments and we pay every balance in full each month. If you do that, the points, hotel upgrades, and built-in insurance can cover a big chunk of a family trip without spending more than you already do. If you carry a balance, interest wipes out the value and it is not worth it.

We started with the Chase Sapphire Preferred and still recommend it as a first card. The annual fee is modest, the points transfer to plenty of airline and hotel partners, and it is a simple way to learn the basics before adding more cards.

It varies a lot by program and property — anywhere from around 5,000 to 50,000 or more points per night. The trick is not the number, it is the value per point: transferring points to the right hotel program often gets you far more than cashing them out for statement credit.

Each new card causes a small, temporary dip at first, but in our case our credit scores actually went up over time. As your total credit limits rise and your balances stay low, your credit utilization drops — and lower utilization generally helps your score. The catch, as always: this only holds true if you never carry a balance.

In our experience, yes. We have had a non-refundable trip refunded, a phone repair covered, and an appliance claim paid — more than 2,000 dollars back across the three. You usually have to file the claim yourself and keep your receipts, but the coverage is real.

With most major travel cards, points do not expire as long as the account stays open and in good standing. Always check the rules for your specific program, but we have never lost points simply by holding our cards.

See exactly which cards we carry With real redemption numbers

Our Wallet →